The retirement landscape of 2026 has become a game of “moving goalposts.” As we saw in the recent Vanguard “How America Saves” report, the average 401(k) balance for those 65 and up is hovering around $299,442. While that sounds like a lot of money, in a 2026 economy where a “modest” retirement is being priced at $4 million, that average balance leaves a staggering $3.7 million gap. This “Wealth Gap” is exactly why thousands of investors are now looking to buy silver online. They aren’t just buying a metal; they are buying a “Tangible Floor” to protect what they have left from the silent tax of inflation. But in a digital world full of “paper” promises and high-tech counterfeits, choosing how and where you buy is the most critical financial decision you will make this decade.

1. Introduction: The 2026 Retirement Reality Check

If you are between the ages of 50 and 65, you are in the “Red Zone.” You no longer have 30 years to recover from a stock market crash or a banking holiday. The data is clear: relying solely on “Paper Wealth” (stocks, bonds, and digital cash) is no longer a complete strategy.

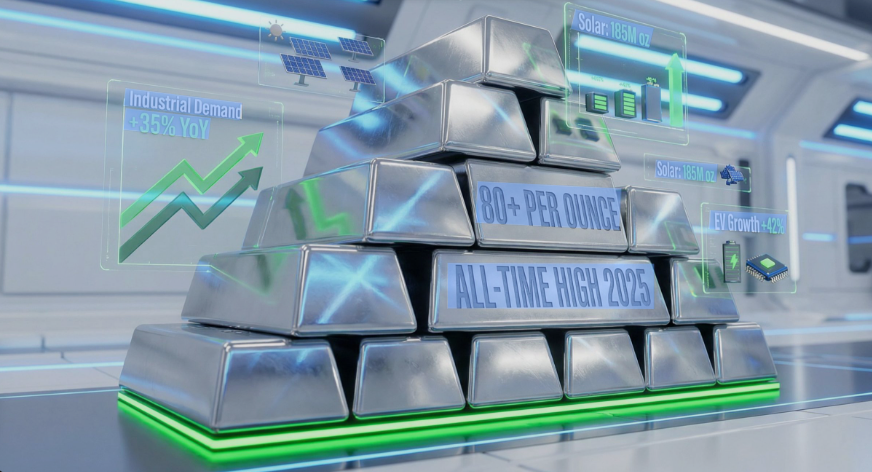

To bridge the gap between your current 401(k) and that $4M “Freedom Number,” you need assets that have no counterparty risk. Silver, currently fueled by a massive AI-industrial supply squeeze, has become the premier choice for those looking to leverage a price hike while maintaining a physical safety net.

2. Key Features to Consider: The “Red Flags” of 2026

When you decide to buy silver online, the internet can feel like a minefield. To protect your hard-earned capital, you must look for these three non-negotiable features:

A. Transparent Pricing (The “Spread” Test)

In 2026, some dealers are charging “stealth premiums” as high as 40% on certain coins. Always check the “Bid/Ask” spread. A reputable dealer should be able to tell you exactly what they will pay you to buy that silver back before you even purchase it.

B. Physical Delivery vs. “Paper” Credits

If a site offers you “silver” but won’t let you take physical delivery or move it to an IRS-approved vault in your name, you aren’t buying silver—you’re buying a receipt. In a systemic crisis, a receipt is worthless.

C. Institutional Reputation

Check the 2026 Better Business Bureau (BBB) and Business Consumer Alliance (BCA) ratings. You are looking for a company that has been through market cycles (like the 2020 crash and the 2024 AI surge) and still maintains a 5-star rating.

3. Top Recommendations: Navigating the 2026 Market

While there are many “retail shops” online, the serious investor—the one looking to secure a $50k to $1M+ portion of their retirement—needs a specialized partner.

Our #1 Choice: Augusta Precious Metals Augusta has separated themselves from the pack in 2026 by refusing to use “fear-mongering” tactics. Instead, they focus on Education. Their Harvard-trained economic team provides a one-on-one web conference that explains how silver acts as a hedge against the exact “Wealth Gap” we see in the Vanguard data. They aren’t just a shop; they are a lifetime service provider for your Silver IRA.

🏛️ IS SILVER THE BEST INVESTMENT IN 2026? The data suggests a major structural shift is happening. Don’t guess with your future. 👉 Download Your Free 2026 Silver Prediction & Price Guide Here

4. Comparison and Analysis: Where Do You Stand?

Let’s look at the “Retirement Reality Check” infographic data. If the average 65-year-old has ~$300k, but needs a “Tangible Floor” of $150k in metals to be truly secure, they are currently 50% under-allocated to hard assets.

The Leverage Factor: By moving a portion of that $300k into a Silver IRA, you aren’t just “saving”—you are positioning yourself to benefit from the industrial silver deficit that the “Paper Market” hasn’t fully priced in yet.

5. Buying Guide: 3 Steps to Your “Tangible Floor”

- Calculate Your Gap: Take your current retirement balance and subtract it from your “Freedom Number.”

- Audit Your Paper: How much of your 401(k) is in “Paper” (stocks) vs. “Hard” (metals/real estate)? In 2026, a 10-20% allocation to physical silver is the standard for high-security portfolios.

- Initiate a “Direct Transfer”: To avoid the 10% IRS penalty, always use a direct custodian-to-custodian transfer when buying silver for an IRA.

6. Final Thoughts: Advice from Marcus Sterling

Marcus’s Advice: The “Millionaire” Mindset

“When I look at the Vanguard data, I don’t see numbers; I see people who are one ‘Black Swan’ event away from a crisis. My advice for 2026 is simple: Don’t wait for the $4M reality to hit you. Whether you have $40,000 or $4,000,000, the goal is the same—convert your ‘uncertain’ paper gains into ‘certain’ physical ounces. When you buy silver online, you are essentially buying time. You are buying the ability to stay retired, no matter what happens to the dollar.” — Marcus Sterling

🏦 SECURE YOUR LEGACY: Ready to see how a Silver IRA can close your retirement gap? 👉 Download the Free Augusta Wealth Protection Report

7. Frequently Asked Questions (FAQ)

Q: Can I really get a Silver IRA if I already have a 401(k)? A: Yes. Most 401(k)s from previous employers, and many current ones, allow for a “tax-free rollover” into a Self-Directed IRA.

Q: Why is the $4M number trending? A: Because of the 2026 “Cost of Living” surge. Financial experts now agree that to maintain a middle-class lifestyle without outliving your money, $4M is the new safe harbor.

Q: Is it better to buy silver bars or coins? A: For an IRA, both are fine as long as they meet the .999 purity requirement. Bars usually have lower premiums, while coins are more “liquid” for smaller trades.

Leave a Reply